Are you dreaming of a big financial future but currently struggling with a small income? This comprehensive guide, “How to Turn a Small Income Into a Big Financial Future,” will provide you with the actionable strategies and proven techniques you need to transform your financial outlook. Learn how to effectively budget, invest, and grow your wealth, even on a limited budget. Discover the secrets to building financial stability, achieving financial freedom, and securing your long-term financial success. Don’t let a small income define your financial destiny; take control and build the future you deserve.

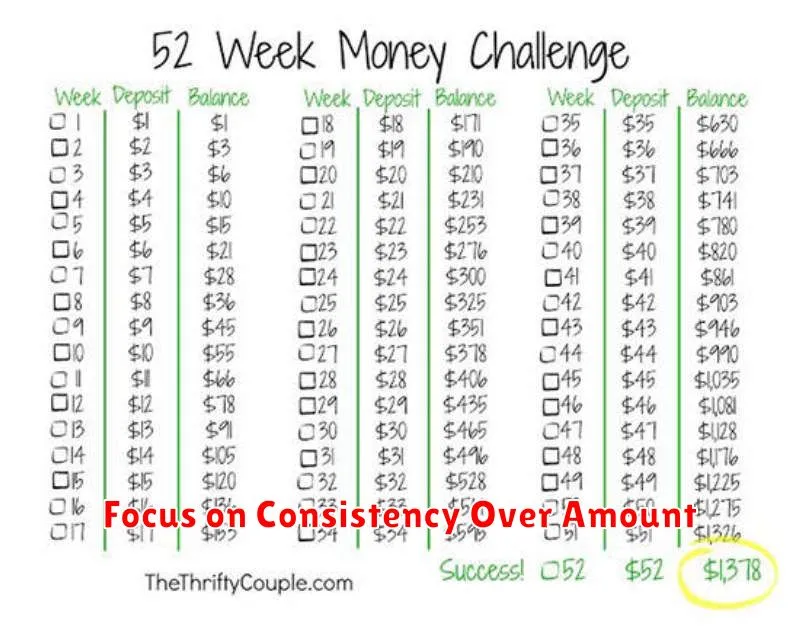

Focus on Consistency Over Amount

Building a substantial financial future doesn’t hinge on earning a massive income immediately. Instead, consistency is key. Small, regular contributions to savings and investments, even with a modest income, compound significantly over time. This consistent approach is far more effective than sporadic large contributions.

Consistency fosters discipline and builds good financial habits. It’s about establishing a routine – automatically transferring a small percentage of your income into savings or investments each month. This automated approach eliminates the temptation to spend that money impulsively. The power of compounding makes even small, consistent contributions grow exponentially over the long term.

Think of it like this: a small stream consistently flowing into a reservoir will eventually fill it, whereas occasional floods might fill it temporarily but then leave it empty again. Choose the consistent stream of savings to secure your financial future.

Therefore, prioritize consistent saving and investing regardless of the amount. Focus on creating a sustainable plan you can maintain, even during lean times. This long-term strategy, while seemingly slow at first, ultimately delivers remarkable financial growth.

Track Every Dollar and Eliminate Waste

Turning a small income into a significant financial future requires meticulous budgeting. The first step is to track every dollar you earn and spend. This involves using budgeting apps, spreadsheets, or even a simple notebook to record all income and expenses.

Once you have a clear picture of your spending habits, you can identify areas of wasteful spending. This could be anything from daily coffee purchases to unnecessary subscriptions. By eliminating these non-essential expenses, you free up funds for saving and investing.

Careful tracking also helps you uncover hidden expenses. You might be surprised at how much money you’re spending on seemingly small things. By reducing these small leaks, you can accumulate significant savings over time.

Remember, even small amounts saved consistently add up. Consistent tracking and elimination of waste are crucial for building a solid financial foundation, regardless of your starting income.

Automate a Small % to Savings Every Payday

Even with a small income, consistent saving is crucial for building a strong financial future. Automating a small percentage of your paycheck into a savings account is a highly effective strategy. This removes the temptation to spend that money and ensures consistent contributions.

Start by determining an affordable percentage to save, even if it’s just 1-5% of your income. Most banks and financial institutions offer automatic transfers that can be set up to deduct this amount from your checking account and deposit it into your savings account each payday. This process requires minimal effort yet delivers significant long-term results.

The power of compound interest will amplify your savings over time. While starting small, the consistent contributions, combined with interest earnings, will steadily grow your savings, laying a solid foundation for future financial goals such as purchasing a home, investing, or covering unexpected expenses.

Consider setting up separate savings accounts for different goals – emergency fund, down payment, etc. This helps you to visually track your progress and stay motivated. Consistency is key. Even small, automated contributions add up significantly over time.

Invest in Yourself First (Skills, Knowledge)

Turning a small income into a large financial future requires strategic investment, and the most crucial investment is in yourself. This means focusing on acquiring new skills and expanding your knowledge base.

Consider pursuing high-demand skills relevant to your career field or an area of interest with high earning potential. This might involve taking online courses, attending workshops, or pursuing certifications. The goal is to increase your marketability and earning capacity.

Beyond technical skills, invest in soft skills like communication, negotiation, and problem-solving. These are universally valuable and enhance your performance in any role, boosting your career progression.

Continuous learning is key. Stay updated on industry trends and advancements through reading, podcasts, and networking. This proactive approach demonstrates initiative and positions you for future opportunities.

Remember that investing in yourself is not just about monetary gain; it’s about personal growth and increased self-confidence, which are vital for achieving long-term financial success.

Use Side Hustles Strategically

Strategic use of side hustles is crucial for transforming a small income into significant financial growth. Don’t just pick any side hustle; choose one that complements your skills and interests, maximizing your efficiency and enjoyment. Careful planning is key: research market demand and potential profitability before investing time and resources.

Prioritize your side hustle based on its potential for scalability and long-term growth. A side hustle with high earning potential, even if initially time-consuming, can generate substantial returns over time. Consider hustles that offer opportunities for automation or delegation as your income grows.

Consistent effort is paramount. Treat your side hustle like a business, setting realistic goals and tracking your progress. Regularly review your strategy, adapting to market changes and personal circumstances. This iterative approach is essential for sustained growth and success.

Reinvent and diversify as needed. As your side hustle evolves, consider expanding your offerings or exploring related opportunities. Diversification minimizes risk and maximizes your income potential. The goal is to build a sustainable system, not just a quick profit.

Finally, remember that financial discipline remains crucial. Save and invest a significant portion of your side hustle earnings to accelerate your financial progress. This disciplined approach will transform your small income into a substantial foundation for your future.

Live Below Your Means With Intention

Living below your means isn’t about deprivation; it’s about intentional spending. It requires a mindful approach to your finances, prioritizing needs over wants and actively seeking opportunities to save.

Create a realistic budget that tracks your income and expenses. Identify areas where you can reduce spending without sacrificing your overall quality of life. This might involve cutting back on subscriptions, finding cheaper alternatives for groceries, or limiting impulse purchases.

Track your progress regularly to stay accountable. Celebrate small victories and adjust your budget as needed. The key is consistency and a long-term perspective. By intentionally living below your means, you’ll build a solid financial foundation and accelerate your path toward a secure financial future, even on a small income.

Remember, this isn’t about permanent sacrifice. It’s about strategic saving that empowers you to achieve your financial goals faster. Once you’ve built a strong financial cushion, you’ll have the freedom to increase your spending in ways that truly align with your values.

Celebrate Milestones and Keep Going

Building wealth from a small income requires patience and persistence. It’s a marathon, not a sprint. Along the way, you’ll achieve significant milestones—paying off debt, reaching a savings goal, or even a small investment profit. Celebrate these wins! Acknowledge your progress and reward yourself appropriately. This positive reinforcement is crucial for maintaining motivation and combating discouragement.

However, celebrations should be modest and brief. Don’t let a small victory derail your long-term financial plan. The key is to acknowledge the accomplishment, appreciate the effort, and then immediately refocus on the next step toward your larger financial goals. This continuous cycle of progress, recognition, and renewed effort is the foundation of building lasting wealth.

Remember, consistent effort, even with a small income, will yield significant results over time. Keep your eyes on the prize, celebrate your wins, and keep moving forward.

{kind=link}