Setting realistic financial goals and actually sticking to them can feel daunting, but it’s achievable with the right approach. This article provides a practical guide to help you define achievable financial goals, create a sustainable budget, and develop effective saving and investing strategies to build a secure financial future. Learn how to overcome common obstacles, stay motivated, and transform your financial aspirations into tangible financial success. Discover the secrets to smart financial planning and achieve your long-term financial objectives.

Differentiate Between Dreams and Actionable Goals

While both dreams and actionable goals involve aspirations, they differ significantly in their characteristics. Dreams are often broad, long-term aspirations, lacking specific details or timelines. They serve as motivating visions but aren’t directly translated into steps. For example, “owning a beach house” is a dream.

Conversely, actionable goals are specific, measurable, achievable, relevant, and time-bound (SMART). They break down larger aspirations into smaller, manageable steps with defined outcomes and deadlines. For instance, “saving $500 per month for five years to contribute towards a down payment on a beach house” is an actionable goal.

The key differentiator lies in tangibility and actionability. Dreams provide inspiration, while actionable goals provide a roadmap to achieve those dreams. Only by transforming dreams into actionable goals can you effectively pursue and attain your financial aspirations.

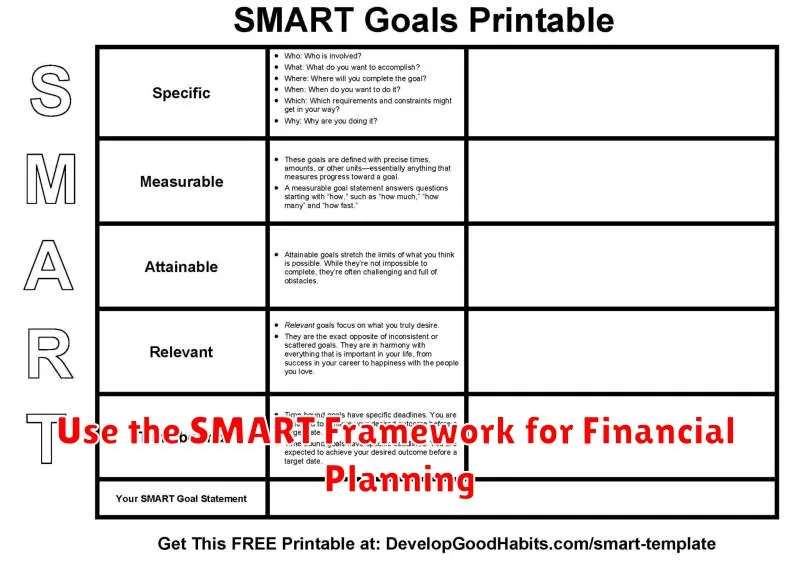

Use the SMART Framework for Financial Planning

Setting realistic financial goals requires a structured approach. The SMART framework provides a valuable tool for achieving this. SMART stands for Specific, Measurable, Achievable, Relevant, and Time-Bound.

Specific goals clearly define what you want to achieve. Instead of “save more,” aim for “save $10,000 for a down payment on a house.” Measurable goals allow you to track your progress. Use quantifiable metrics like dollar amounts or percentages.

Achievable goals are realistic given your current financial situation and resources. Set ambitious yet attainable targets. Relevant goals align with your overall financial objectives and life aspirations. Ensure your goals contribute to your larger financial picture.

Finally, Time-Bound goals establish a deadline. Setting a timeframe creates urgency and helps you stay focused. For example, “save $10,000 for a down payment within two years.” By using the SMART framework, you can create financial goals that are both challenging and attainable, significantly increasing your chances of success.

Break Down Big Goals into Mini Milestones

Achieving significant financial goals, like buying a house or paying off debt, can feel overwhelming. Breaking down these large objectives into smaller, manageable milestones is crucial for maintaining motivation and tracking progress. Instead of focusing on the distant, daunting end goal, concentrate on achievable steps along the way.

For example, if your goal is to save $50,000 for a down payment, don’t just aim for that final number. Instead, set mini-milestones such as saving $5,000 in the first year, then another $10,000 in the second, and so on. These smaller victories will provide a sense of accomplishment and keep you engaged in the process.

Clearly define each milestone with a specific target amount and a realistic deadline. This allows you to monitor your progress effectively and make adjustments to your plan as needed. Regularly reviewing your mini-milestones, perhaps monthly or quarterly, helps stay on track and identify any potential roadblocks early on.

Remember, the key is to create realistic and attainable milestones. Setting overly ambitious targets can lead to discouragement and ultimately hinder your progress toward your larger financial goal. By celebrating each milestone achieved, you build momentum and maintain the motivation to reach your ultimate objective.

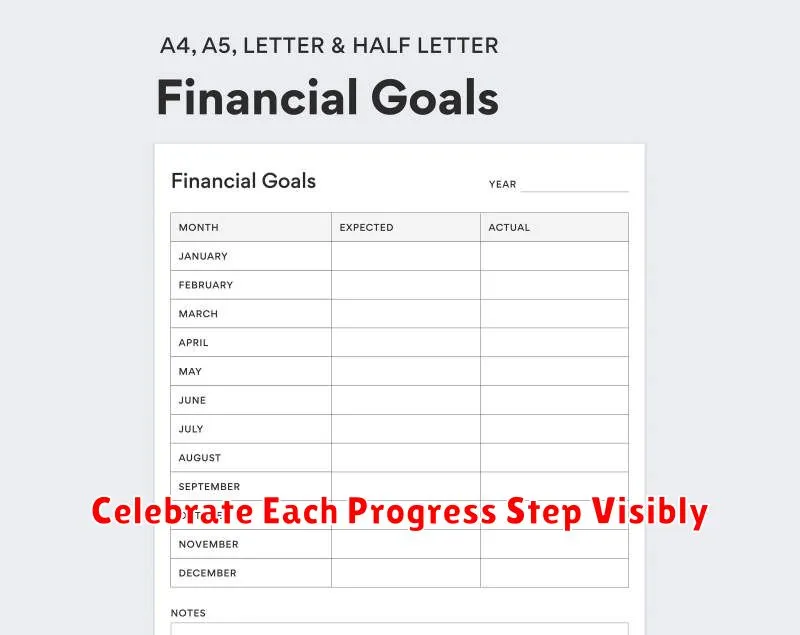

Celebrate Each Progress Step Visibly

Reaching financial goals requires consistent effort and can be a long journey. To maintain motivation and prevent discouragement, it’s crucial to visibly celebrate each milestone achieved. This doesn’t necessitate extravagant celebrations; small, meaningful acknowledgments are sufficient.

Consider tracking your progress using a visual aid like a chart or a progress bar. As you reach smaller goals along the way – paying off a credit card, saving a specific amount – mark your accomplishment prominently. This visual representation reinforces your success and provides a tangible sense of accomplishment.

Reward yourself appropriately. This could be a small treat, a relaxing activity, or even simply taking time to acknowledge your hard work. The key is to associate positive feelings with your financial progress, strengthening the habit and motivating you to continue.

By acknowledging every step forward, you cultivate a positive reinforcement loop. This positive feedback boosts morale, making the overall journey more enjoyable and sustainable. You’ll find yourself more likely to stay committed to your financial goals when you actively celebrate each step.

Keep a Visual Reminder of Your Top Goal

Maintaining focus on your financial goals is crucial for success. A powerful technique is to create a visual reminder of your top priority. This could be a sticky note on your mirror, a photo of your desired outcome (e.g., a house, a car), or a digital wallpaper on your phone or computer. The key is choosing a method that you’ll see frequently, reinforcing your commitment throughout the day.

This constant visual cue serves as a potent motivational tool. When faced with tempting expenditures, the reminder subtly steers you back towards your primary financial objective. By consistently seeing your goal, you’ll be more likely to make choices aligned with achieving it. Regularly reviewing and updating your visual reminder ensures it remains relevant and engaging.

Consider the impact of a visual representation of your dream on your daily decision-making. The simple act of seeing your goal can significantly enhance your discipline and perseverance, thus improving your chances of achieving your financial aspirations.

Review and Adjust Monthly with Journal Reflections

Regularly reviewing your progress is crucial for achieving realistic financial goals. A monthly review allows you to track your spending, identify areas needing improvement, and make necessary adjustments to your budget.

Journaling plays a vital role in this process. By documenting your financial activities, thoughts, and feelings, you gain valuable insights into your spending habits and emotional responses to money. This self-reflection helps you understand the why behind your financial decisions, leading to more informed choices.

During your monthly review, compare your actual spending against your planned budget. Analyze any discrepancies. Did unexpected expenses arise? Did you overspend in certain categories? Your journal entries will provide context, helping you identify patterns and make data-driven adjustments to your plan.

This reflective process fosters accountability and reinforces your commitment to your financial goals. By consistently reviewing and adjusting your plan based on your journal reflections, you increase your chances of success significantly.

Avoid Goal Fatigue by Keeping It Simple

Goal fatigue is a real phenomenon. Setting overly ambitious or numerous financial goals simultaneously can lead to overwhelm and ultimately, failure to achieve any of them. This is counterproductive and demotivating.

To avoid this, focus on simplicity. Start with one or two realistic and achievable goals. For example, instead of aiming to pay off all debt, buy a house, and max out retirement contributions this year, prioritize paying off high-interest debt first. This single, manageable goal provides a sense of accomplishment and momentum.

Specificity is key. Instead of vaguely aiming to “save more,” set a concrete goal like “save $500 per month for a down payment.” Breaking down large goals into smaller, more achievable steps also helps maintain motivation and prevent feeling overwhelmed. Regularly review and adjust your goals as needed to ensure they remain relevant and attainable.

By keeping your financial goals simple, you’ll experience less stress and a greater likelihood of achieving them. Remember, consistent progress, even on small goals, is far more effective than sporadic efforts on many ambitious targets.

{kind=link}