Facing unexpected expenses can be a daunting experience, triggering feelings of panic and financial instability. This article provides a practical guide on how to effectively manage unexpected costs without succumbing to stress. We will explore proven strategies for handling emergency expenses, building a robust emergency fund, and navigating the challenges of unforeseen financial burdens. Learn how to regain control of your finances and develop a resilient approach to unexpected life events.

Create a Small Emergency Fund as Your First Shield

Unexpected expenses can trigger significant financial stress. A crucial first step in handling these situations without panic is establishing a small emergency fund. This acts as your initial defense against unforeseen costs.

Start small; even $500 can provide a buffer against minor emergencies like a sudden car repair or unexpected medical bill. The goal isn’t to amass a large sum immediately, but to build a habit of saving consistently.

Regular contributions, even small amounts, are key. Automate transfers from your checking account to a separate savings account designated solely for emergencies. This ensures consistent growth without requiring constant manual effort.

Once your initial goal is reached, continue contributing to increase your financial resilience. The peace of mind provided by having emergency funds surpasses the immediate need for the money itself.

Consider your personal financial situation and set a realistic savings target. The sense of security an emergency fund provides is invaluable in navigating unexpected expenses calmly and effectively.

Separate ‘Emergency’ from ‘Inconvenience’ Spending

Unexpected expenses can trigger panic, but a crucial first step is distinguishing between true emergencies and mere inconveniences. Emergencies are unforeseen events requiring immediate action to protect health, safety, or essential assets – like a medical bill, car repair impacting daily commute, or home system failure. These demand immediate attention and resource allocation.

Inconveniences, on the other hand, are unexpected costs that disrupt convenience but don’t pose an immediate threat. Examples include a broken appliance (if you have alternatives), a minor car scratch, or an unplanned social event expense. While inconvenient, these can often be addressed through adjustments to your budget or delayed without significant repercussions.

Clearly differentiating between these categories helps prioritize spending. Addressing emergencies first is paramount, ensuring necessary safety and functionality. Inconveniences can often wait until funds are available or alternative solutions are explored, preventing impulsive overspending during stressful situations. This clear separation reduces financial anxieties and promotes more effective financial management during unexpected events.

Pause Non-Essential Spending Temporarily

Facing an unexpected expense can be stressful, but a quick and effective first step is to immediately pause all non-essential spending. This means temporarily cutting back on discretionary items.

Identify what constitutes non-essential spending in your budget. This might include dining out, entertainment, subscriptions, online shopping, or impulse buys. Creating a clear list will help you stay focused.

Prioritize essential expenses such as housing, utilities, food, and transportation. By temporarily forgoing non-essential purchases, you can free up funds to cover the unexpected cost and prevent further financial strain.

This temporary pause allows you to assess the situation and develop a more comprehensive plan for managing the unexpected expense without resorting to high-interest debt. Remember, this is a temporary measure designed to provide immediate financial relief.

Prioritize Expenses Using the Needs Pyramid

When faced with unexpected expenses, prioritizing is crucial. The Needs Pyramid offers a structured approach. At the base are your essential needs: shelter, food, utilities, and transportation. These are non-negotiable and should be covered first.

The next level encompasses essential services like healthcare and debt repayments (especially high-interest ones). These are vital for long-term well-being and financial health. Addressing these minimizes future financial strain.

Above that are needs that improve your quality of life, such as education or childcare. These are important, but can often be temporarily adjusted or postponed during financial hardship. Consider if they can be reduced or eliminated for a short time.

Finally, at the top are wants – entertainment, dining out, non-essential shopping. These are the first to be cut when dealing with unexpected costs. Remember, this is temporary; you can resume these later.

By using the Needs Pyramid, you can effectively allocate your resources, focusing on essential needs first and making informed decisions about which expenses to reduce or delay. This structured approach will help navigate unexpected financial challenges without panic.

Negotiate Flexible Payment Plans If Needed

Facing an unexpected expense that threatens your budget? Don’t panic. Negotiating a flexible payment plan with creditors can provide much-needed breathing room. This involves contacting the relevant party (e.g., medical provider, credit card company, landlord) and explaining your situation honestly.

Clearly articulate your financial difficulty, emphasizing your intention to pay the debt in full. Propose a realistic payment schedule that aligns with your income and budget. Be prepared to provide documentation supporting your financial situation if requested. Remember to get the agreement in writing to avoid future misunderstandings.

Many companies are willing to work with customers experiencing financial hardship. A proactive approach, demonstrating your commitment to repayment, significantly increases your chances of successfully negotiating a flexible payment plan. This strategy allows you to manage unexpected expenses responsibly and avoid further financial stress.

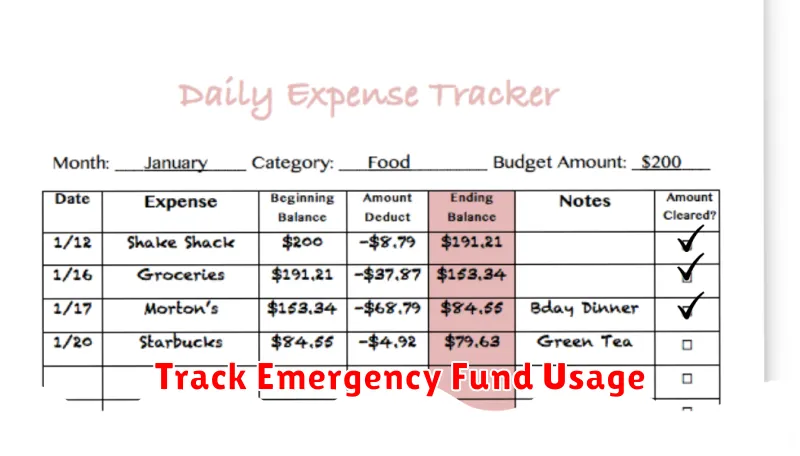

Track Emergency Fund Usage

Maintaining a detailed record of emergency fund usage is crucial for responsible financial management. Accurate tracking allows you to understand your spending patterns and identify areas for potential improvement in future budgeting.

Use a spreadsheet or a dedicated budgeting app to meticulously log each withdrawal. Include the date, the amount withdrawn, and a clear description of the expense. This provides a transparent history of your emergency fund activity.

Regularly review your tracking records. This allows you to monitor the fund’s balance and assess its ability to cover future unexpected expenses. Promptly replenish the fund after each withdrawal to maintain its protective capacity.

By diligently tracking your emergency fund usage, you foster financial awareness, prevent overspending, and ensure the fund remains a reliable safety net for unforeseen circumstances.

Learn and Adjust to Prevent Future Shocks

Unexpected expenses can be stressful, but proactive learning and adjustment can significantly reduce their impact. Financial literacy is key; understanding budgeting, saving, and investing allows for better preparedness. Regularly reviewing your budget and identifying areas for improvement helps you allocate resources effectively.

Building an emergency fund is crucial. Aim for 3-6 months’ worth of living expenses to cover unforeseen situations. This fund acts as a buffer against unexpected costs, preventing you from resorting to high-interest debt.

Regularly assessing your insurance coverage is vital. Ensure you have adequate health, home, and auto insurance to mitigate potential large expenses. Understanding your policy’s coverage limits and deductibles helps you plan accordingly.

Developing good financial habits – like tracking expenses, avoiding unnecessary spending, and prioritizing saving – is a long-term strategy to build resilience against future financial shocks. By consistently learning and adapting your financial practices, you can create a more secure financial future and navigate unexpected expenses with greater ease.

{kind=link}