Understanding the psychology of impulse spending is crucial for regaining control of your finances. This article delves into the underlying cognitive biases and emotional triggers that lead to unplanned purchases, examining how marketing techniques exploit these vulnerabilities. We’ll explore practical strategies and effective techniques to curb impulsive buying and develop healthier spending habits, ultimately empowering you to achieve greater financial stability and reduce financial stress.

Understand the Emotional Triggers Behind Impulse Buys

Impulse buying is rarely a purely rational decision; it’s heavily influenced by emotional triggers. Understanding these triggers is crucial to controlling impulsive spending.

Stress and anxiety often lead to impulsive purchases as a form of self-soothing or distraction. The temporary pleasure derived from acquiring something new can provide a fleeting sense of relief.

Sadness or loneliness can also fuel impulse buying. Individuals may seek to fill an emotional void or alleviate feelings of isolation through material possessions.

Boredom can similarly trigger impulsive spending. The act of shopping itself, even without a specific purchase in mind, can provide a temporary distraction and sense of engagement.

Low self-esteem can contribute to impulse buying as individuals may attempt to boost their self-image or seek external validation through purchases.

Fear of missing out (FOMO), fueled by social media and marketing, can create a sense of urgency, leading to unplanned purchases.

Rewarding oneself, even for minor achievements, can easily escalate into frequent impulsive spending if not carefully managed.

Recognizing these emotional drivers is the first step towards developing strategies to curb impulsive spending habits.

Track Every Purchase for 7 Days

One effective technique to understand your spending habits and curb impulse purchases is to meticulously track every single purchase you make for a week. This isn’t about judgment; it’s about gaining awareness.

Use a notebook, a spreadsheet, or a budgeting app to record everything: that coffee, the magazine, the unexpected online purchase. Note the amount spent, the item purchased, and, most importantly, the underlying emotion or trigger that led to the purchase (e.g., boredom, stress, reward).

After seven days, review your records. Look for patterns. You might be surprised by how many small, seemingly insignificant purchases add up. This exercise provides invaluable insight into your spending triggers, empowering you to make more conscious choices in the future.

This simple act of tracking lays the groundwork for developing strategies to manage your impulsive spending. It’s the first step towards greater financial control and a healthier relationship with money.

Avoid Shopping When You’re Hungry, Tired, or Bored

Impulse spending is often linked to our emotional state. When we’re hungry, tired, or bored, our self-control weakens. This makes us more susceptible to temptation and less likely to make rational purchasing decisions.

Hunger can lead to cravings and impulsive food purchases, but it can also extend to non-food items. A low blood sugar level can impair judgment and increase the desire for immediate gratification.

Fatigue similarly impacts our cognitive functions. When tired, we’re less likely to carefully consider purchases and more prone to making quick, unplanned decisions. The effort involved in resisting temptation is simply too high.

Boredom can also trigger impulse buying as a way to seek stimulation or alleviate feelings of emptiness. Shopping offers a temporary distraction, but often leads to regret later.

To combat this, it’s crucial to recognize these triggers and actively avoid shopping when you’re experiencing them. Instead, focus on addressing the underlying need: eat a meal, rest, or find a more fulfilling activity.

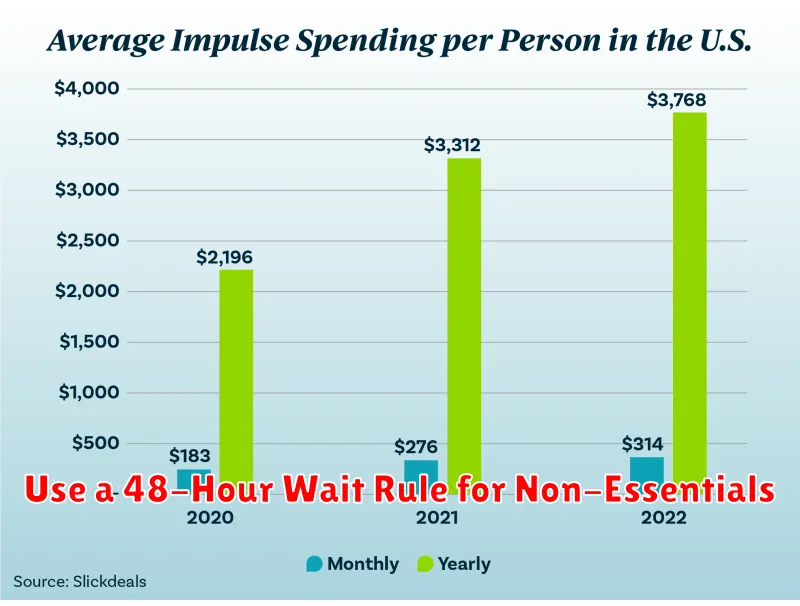

Use a 48-Hour Wait Rule for Non-Essentials

Impulse spending often stems from emotional responses rather than rational needs. A powerful technique to combat this is the 48-hour wait rule. Before purchasing any non-essential item, commit to waiting 48 hours.

This delay provides crucial time for the initial emotional urge to subside. After two days, reassess your desire. If you still feel strongly about the purchase, proceed. However, in many instances, the urgency will fade, revealing the purchase as unnecessary.

This simple rule creates a buffer between the impulse and the action, allowing for a more thoughtful and deliberate decision-making process. By consciously implementing the 48-hour wait rule, you can significantly reduce your impulse spending and improve your financial well-being.

Set Spending Limits on Debit/Credit Cards

One effective strategy to combat impulse spending is to set spending limits on your debit and credit cards. This involves pre-determining a maximum amount you’ll spend each day, week, or month on specific categories (e.g., groceries, entertainment, clothing). By setting these limits, you create a psychological barrier that helps prevent overspending.

Many banks and credit card companies offer tools to assist with this, including spending alerts and the ability to set transaction limits. Utilize these features to receive immediate notifications when you approach your predetermined spending limits, prompting you to reconsider unnecessary purchases.

Consider using a budgeting app to track your spending against these limits. These apps provide a clear visual representation of your spending habits, helping you understand where your money is going and identify areas where you can cut back. Regularly reviewing your spending against your set limits promotes mindful spending and strengthens your ability to resist impulsive purchases.

Remember, the key is to set realistic limits that align with your financial goals and lifestyle. Start by tracking your current spending to establish a baseline, then gradually adjust your limits as needed. Consistency in adhering to these limits is crucial for long-term success in controlling impulse spending.

Unsubscribe from Retail Emails and Alerts

A significant contributor to impulse spending is the constant bombardment of retail emails and alerts. These messages, often employing persuasive techniques and highlighting limited-time offers, trigger our fear of missing out (FOMO) and exploit our psychological vulnerabilities.

Unsubscribing from these emails is a powerful first step in controlling impulse spending. By removing the constant visual reminders of sales and new products, you significantly reduce the chances of making unplanned purchases. This simple action creates psychological distance between you and tempting offers, allowing for more rational decision-making.

Consider unsubscribing from all but the most essential retailers. This will drastically reduce the number of promotional messages in your inbox, leading to a more peaceful and financially responsible online experience. This proactive approach directly addresses a key trigger for impulsive buying behavior.

Replace Shopping Habits with Positive Alternatives

Understanding the psychology behind impulse spending is crucial to breaking the cycle. Often, shopping acts as a coping mechanism for stress, boredom, or low self-esteem. Replacing this habit requires identifying your triggers and developing healthier alternatives.

Instead of immediately reaching for your credit card, try engaging in activities that provide a similar emotional reward without the financial burden. Mindfulness practices like meditation or deep breathing can help manage stress. Creative hobbies such as painting, writing, or playing music can offer a sense of accomplishment and self-expression. Social interaction with loved ones can combat loneliness and boost your mood.

Physical exercise releases endorphins, creating a natural mood boost. Spending time in nature offers a sense of calm and perspective. Learning new skills, through classes or online resources, fosters personal growth and a sense of purpose. By consciously choosing these positive alternatives, you can gradually shift your reliance on shopping for emotional gratification.

Remember that changing ingrained habits takes time and effort. Patience and self-compassion are key. Don’t get discouraged by occasional setbacks; instead, use them as learning opportunities to refine your strategies and reinforce your commitment to a healthier relationship with spending.

{kind=link}