Are you worried about falling into a debt trap? Many people unknowingly make everyday mistakes that lead to overwhelming debt. This article will explore common pitfalls, such as overspending, neglecting budgeting, and ignoring high-interest credit card debt. Learn how to avoid these financial mistakes and take control of your finances to build a secure financial future, free from the burden of unmanageable debt.

Living Above Your Means: A Slippery Slope

Living above your means, spending more than you earn, is a major contributor to debt traps. This seemingly small discrepancy between income and expenditure quickly escalates. Initially, it might be covered by savings or credit cards, creating a false sense of security.

However, consistent overspending depletes savings and increases reliance on credit. High-interest debt accumulates rapidly, making it increasingly difficult to catch up. This cycle can lead to a vicious cycle of borrowing to pay off existing debts, further exacerbating the financial burden.

Careful budgeting and tracking expenses are crucial to avoid this slippery slope. Understanding where your money is going allows for informed financial decisions and helps curb impulsive spending. Prioritizing needs over wants and setting realistic financial goals are essential steps in achieving financial stability and avoiding the pitfalls of living beyond your means.

Using Credit for Wants Instead of Needs

One of the most common pitfalls leading to debt is using credit for wants instead of needs. A need is something essential for survival or well-being, like food, shelter, or medical care. A want is something desirable but not essential, such as a new phone, a vacation, or designer clothes.

Using credit for wants often leads to accumulating high-interest debt that can be difficult to manage. The interest charges quickly add up, making the initial cost of the purchase far more expensive than it initially seemed. This can create a vicious cycle of debt, where you’re constantly paying interest and struggling to make minimum payments.

To avoid this, carefully distinguish between your needs and wants. Prioritize needs and consider saving for wants before purchasing them with credit. This ensures responsible spending habits and prevents the accumulation of unnecessary debt.

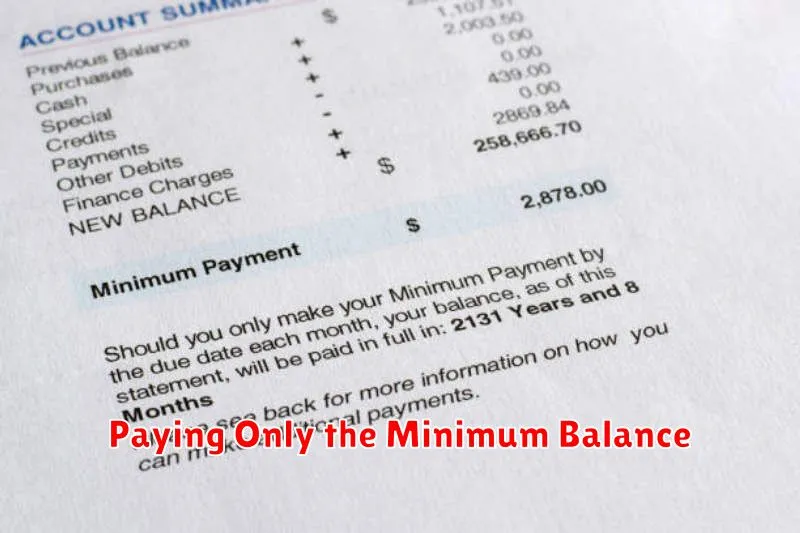

Paying Only the Minimum Balance

Paying only the minimum balance on your credit cards is a major mistake that can quickly lead to a debt trap. While it might seem convenient in the short-term, it significantly increases the amount of interest you pay over time. This is because the majority of your payment goes towards interest, leaving only a small portion to reduce your principal balance.

The high interest rates on credit cards compound rapidly, meaning you pay interest on your interest. This snowball effect can make it incredibly difficult to pay off your debt, even if you diligently pay the minimum each month. The longer it takes to pay off the debt, the more you’ll pay in total.

To avoid this trap, prioritize paying more than the minimum payment each month. Aim to pay at least the full amount of new purchases made during the month, and allocate any extra funds towards paying down the principal balance. Consider creating a budget to help manage your spending and ensure you can make larger payments towards your debt.

Not Tracking Small Loans from Friends or Apps

One common oversight leading to debt traps is the failure to meticulously track small loans, whether from friends or lending apps. These seemingly insignificant amounts can quickly accumulate, creating an overwhelming debt burden if not carefully monitored.

Accurate record-keeping is crucial. Maintain a detailed log of each loan, including the amount borrowed, the lender’s name, the repayment date, and the payment method. This simple step provides clarity and helps avoid misunderstandings and strained relationships.

Utilizing budgeting apps or spreadsheets can streamline the tracking process. These tools offer efficient ways to record transactions and set reminders for repayment deadlines, preventing missed payments and accumulating late fees.

Ignoring these small loans can have significant consequences. Overlooking repayment schedules can damage personal relationships and negatively impact your credit score, even if the amounts are relatively small. Proactive tracking prevents these negative outcomes.

Missing Due Dates and Paying Late Fees

Failing to meet payment deadlines is a common pitfall leading to debt. Even seemingly small late fees accumulate rapidly, significantly increasing the total amount owed.

Missed payments also negatively impact your credit score, making it harder to secure loans or credit cards in the future with favorable terms. This can create a vicious cycle, trapping you in a spiral of debt.

To avoid this, establish a system for tracking due dates. Use a calendar, planner, or budgeting app to set reminders. Consider setting up automatic payments to ensure on-time payments.

Proactive budgeting and careful financial planning are essential to ensure you have sufficient funds available to meet your payment obligations on time.

Relying on ‘Buy Now, Pay Later’ Offers Too Often

Buy Now, Pay Later (BNPL) services offer a tempting solution for immediate purchases, but over-reliance can quickly lead to debt traps. The convenience often masks the potential for accumulating significant debt if multiple BNPL plans are used concurrently or payments are missed.

Missed payments incur hefty late fees and negatively impact your credit score, making future borrowing more difficult and expensive. The seemingly small amounts spent on each purchase can quickly add up, exceeding your budget and creating a cycle of debt.

To avoid this, practice financial discipline. Carefully consider whether you truly need the item and can afford it upfront. If not, delay the purchase. If you must use BNPL, restrict yourself to one or two plans and diligently track your payments to avoid missed deadlines and accumulating interest.

Ignoring Your Total Debt Picture

One of the biggest mistakes people make when dealing with debt is ignoring the big picture. Focusing solely on individual debts, like paying down a credit card while neglecting a larger loan, can be detrimental. A holistic view of your total debt, including all loans, credit cards, and other obligations, is crucial.

Understanding your overall debt burden allows you to prioritize payments effectively. This involves calculating your debt-to-income ratio (DTI) and identifying high-interest debts that need immediate attention. Without this comprehensive view, you risk falling into a cycle of minimum payments, accruing more interest, and delaying your path to financial freedom.

Creating a detailed debt inventory is the first step. List each debt, including the balance, interest rate, and minimum payment. This allows for a strategic approach to repayment, such as focusing on the highest-interest debt first (debt avalanche method) or tackling the smallest debt first to build momentum (debt snowball method).

Ignoring the total debt picture leads to inefficient repayment strategies, increased interest payments, and prolonged debt struggles. A comprehensive understanding of your debt landscape is essential for creating a successful and effective debt management plan.

{kind=link}